Debt-Free by August 2029: Our Payoff Plan

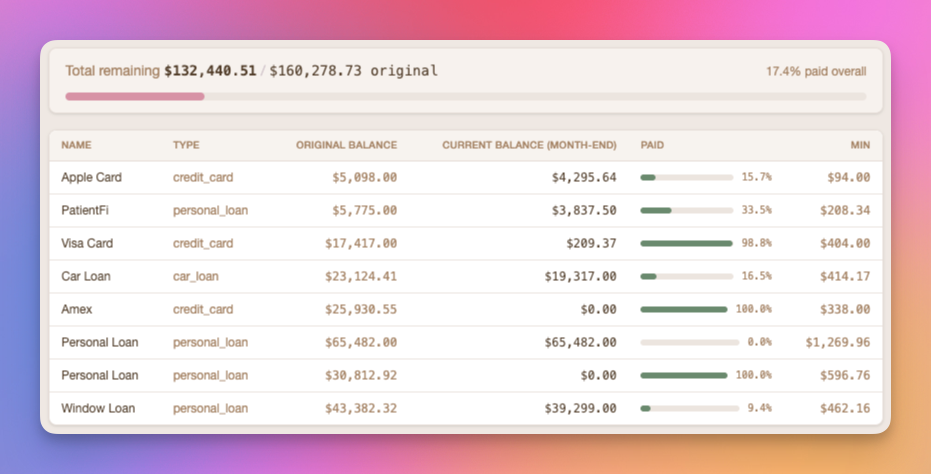

We owed $132,441 across six debts. Not student loans, not business debt, just the regular kind of mess that happens when you stop paying attention for a few years. Home repairs, medical bills, a car, and new windows we absolutely did not budget for. Here's exactly how we're getting out.

Why We Chose a Hybrid Method

Most debt payoff advice tells you to pick a side. Dave Ramsey says snowball, which means paying off your smallest balance first for the psychological win. The math people say to avalanche, which means paying off the highest-interest debt first because you'll save more money overall.

We're doing both. Not because we couldn't commit, but because our debt situation doesn't fit cleanly into either bucket.

Before I explain, some context. Our household income is about $13,600/month from three sources: my husband's W-2, his military disability, and my salary. I also bring in around $1500/month from freelance work. We're not struggling to make ends meet. We're paying a lot in debt payments every month, and we want those payments to go toward our future instead of someone else's interest income.

Here's why a pure method didn't work for us.

Pure snowball would have us paying off the PatientFi line of credit first, then the Apple Card, then USAA Card, and eventually working up to the big ones. The problem is that PatientFi is at 0% interest. Paying it off early saves us nothing. Meanwhile, the USAA Card is 15.6% and the Apple Card sits at 14.49% APR, bleeding money every month.

Pure avalanche would have us throwing everything at the USAA credit card (15%), then the Apple Card (14%), then the USAA consolidation loan (11.4%). The problem there is that the USAA loan is massive ($65k). If we attacked that first, we'd spend two years staring at five other debts with no visible progress.

So we picked based on two rules:

- ★ Kill small debts first to reduce the number of payments we're juggling

- ★ When balances are close, pick the higher interest rate

The goal isn't just being debt-free. It's consolidating down to fewer debts, so when we start the real snowball on the big three, each payoff frees up money.

The Full Debt Breakdown

A quick note on the USAA Consolidation Loan. That $65k used to be three separate debts: an AMEX card, our USAA credit card, and an older USAA loan. All three were at rates between 14% and 21%. We consolidated them into a single loan last month at 11.45%. It feels painful to have a single giant number, but the math is significantly better than before.

A quick note on the USAA Consolidation Loan. That $65k used to be three separate debts: an AMEX card, our USAA credit card, and an older USAA loan. All three were at rates between 14% and 21%. We consolidated them into a single loan last month at 11.45%. It feels painful to have a single giant number, but the math is significantly better than before.

The GreenSky loan is for the windows we financed for our house in 2025. We got them done, and we've barely made a dent in the balance a year later. That one stings.

The Payoff Order

Here's the order we're attacking, with how long each will take at our current plan:

1. USAA Credit Card: Paying the full $209 in May.

2. Apple Card: Putting $2,300/month at this until it's gone. At 14.49%, it's our second-highest rate, and at $4,295 we can wipe it out in two months. This is the biggest psychological win on the list.

3. Patient Fi: 0% interest, so no urgency from a math standpoint. But the minimum is $388/month, and once it's paid off, that $388 rolls into the next debt.

4. Car Loan: $19,317 at 7.74%. Once Apple and Patient Fi are gone, we roll all that money into the car. Five months of focused payments, and the car is paid off. Cars are depreciating assets, and we don't like owing any money on it.

5. GreenSky: The painful windows loan. By the time we get here, we've rolled up every previous payment, so we're throwing around $2,800/month at it. Eleven months and we're done.

6. Debt Consolidation Loan: The big one. By the time all other debts are gone, we'll be sending about $4,100/month toward this loan. It takes about 11 months to wipe out what's left.

Debt-free: August 2029.

Monthly Income Allocation

Here's where the money actually goes. These are the real planned numbers for May 2026.

Income: $14,443/month (combined, after taxes)

- Doug's W-2: $6,513

- My Ardor salary: $4,637

- Doug's disability: $2,493

- Freelance (Baronfig + MacPac): $800

Essentials: $6,924 (48%)

- Mortgage: $4,200

- Utilities (gas, water, electric, internet, phones): $591

- Insurance (life, car, health): $932

- Groceries: $1,000

- Gas & tolls: $200

Debt: $5,043 (35%)

- Minimums on all six debts: $2,837

- Extra attack fund: $2,206

Spending/Fun: $1,550 (11%)

- Each family member gets $100 in personal spending

- Kids' sports: $450

- Restaurants and drinks: $400

- Misc spending buffer: $300

Sinking funds: $360 (2.5%)

This covers all the small recurring bills that aren't tied to a single month.

Savings: $500 (3.5%)

- Emergency fund: $100 (we already have a $1,000 starter buffer, keeping it topped up)

- Gift savings: $400 (birthdays, Christmas, so we're not caught flat)

Leftover: $66. Every dollar has a job.

The Income Sources Funding the Payoff

This is the question people actually want answered.

Our W-2 income and disability ($13,643/month) covers essentials, minimums, fun money, subscriptions, and basic savings. That's everything except the attack fund.

The $2,206 going to the Apple Card every month comes from the freelance income and whatever buffer we've built into the W-2. My contract work isn't glamorous money (~$1,500 a month combined before taxes), but it's the difference between "we're slowly paying off debt" and "we're done in 39 months." Without that freelance income, we'd be looking at a timeline closer to 6 years instead of 4.

I also get three paychecks from my day job in May and October because I'm paid biweekly. That's an extra ~$2,300 twice a year. I don't budget it in; I treat it as an automatic bonus payment straight to debt.

We could technically get out of debt faster if I ramped up content income again. Nora Conrad was earning real money in 2024 before I let it go dormant. Rebuilding that is part of the plan, but I'm not including theoretical future income in an actual payoff timeline. If content income returns, great. If it doesn't, this plan still works.

Timeline to Debt-Free

39 months. August 2029.

That assumes no income drops, no major emergencies, and that we stick to a $1,500 attack fund every single month. Real life doesn't always work like that. With our subscription fund and our sinking fund, we should be able to negate any emergencies that come up. This timeline doesn't include the extra income payments and any bonuses that we get, so we're hopeful that this number will shrink instead of grow

Here's what the arc looks like:

- By end of 2026: Two smallest credit card debts gone, Patient Fi gone, car loan halfway paid

- By end of 2027: Car loan gone, GreenSky halfway paid

- By end of 2028: Everything but the loan gone, final push happening

The thing that actually changes the timeline isn't discipline. It's income. If I pick up a fourth freelance client or content income comes back, we shave months off. If I lose a freelance contract, we lose a few months. The budget is solid. The variable is how much attack money we can put in.

What Could Derail the Plan

This is where most debt payoff posts get dishonest. Here are the things I'm actually worried about.

Losing freelance income. My contracts aren't guaranteed. If one or both dry up, the attack fund drops by $800/month and the timeline pushes out to roughly 46 months instead of 39.

A kid emergency. Two kids, two dogs, two cats, and a house. Something will break. My $1,000 emergency fund, gift savings plus sinking funds give us a cushion for small stuff. A major medical bill or home repair would mean temporarily drawing from the attack fund.

A car problem. The car we're paying off is my car. It's reliable now. It won't be forever. If something happens to Doug's vehicle, we're in trouble too.

The plan for all of these: pause the extra attack payments temporarily, cover the emergency, and resume as soon as possible. We don't stop paying minimums, we don't take on new debt, we just slow down the aggressive payoff. A derailed plan is still a plan. Quitting is the only thing that actually breaks it.

The System Behind It

I track all of this in EveryDollar and a Supabase-backed dashboard I built myself. I also use a Google spreadsheet to track our end-of-month assets, liabilities, and incomes. Every line item, every dollar, is assigned before the month starts.

Four metrics I actually watch:

- ★ Total balance across all debts (down from $135k six months ago)

- ★ Number of active debts (six now, three by the end of the year)

- ★ Interest paid per month (currently around $900, dropping every time a debt falls off)

- ★ Months to debt-free (39 and counting down)

One thing that's changed my relationship with this: we're training ourselves to spend $4,000+/month on debt. When the debt is gone, that money doesn't disappear into lifestyle creep. It rolls into the mortgage (we want to pay it off aggressively, too) and investments. Getting used to the big payments now is the whole point. The habit outlasts the debt.

Side note: I didn't include my third-paycheck months in the budget above. Because I'm paid biweekly, I get an extra paycheck in May and October every year. That's about $2,300 each time. It all goes straight to debt, but I don't plan for it in the monthly budget because it'd throw off the baseline. Consider it a twice-a-year bonus accelerator.

If you want to see the actual spreadsheet setup or ask a question about any of this, the newsletter is the best place to reach me.